After delivering your products or services and wrapping up the job, you simply send out your invoices to your customers just like you normally do.

Step 2

Access cash before invoices are paid

Once you've sent invoices to your Australian business customers, you gain instant access to funds via your invoice finance facility.

Step 3

Your customers pay their invoices

Your customers settle their invoices, and the funds land in the dedicated account created for your invoice finance facility.

Step 4

Funds are released to you

Once your customer payments have arrived, your invoice finance facility is repaid, and the remaining cash is released to you, minus any interest or fees.

Invoice finance is a practical solution for a wide range of Australian businesses. If your cash is tied up in invoices that won’t be paid for 30, 60 or even 90 days, Invoice Finance can bridge the gap.

While Invoice Finance can be a great fit for any business that invoices other Australian businesses on credit terms, Invoice Finance could be the right fit, it’s particularly useful for industries where payment delays are common, such as:

Labour hire and recruitment. Meet payroll obligations while waiting for client payments.

Transport and logistics. Cover fuel, fleet and maintenance costs without delay.

Manufacturing and wholesale. Free up working capital to buy stock and materials.

Security services. Pay security guards, maintain equipment, and meet compliance costs without waiting on long-term client contracts.

No matter the size of your business, if you invoice other businesses after goods or services are delivered, Invoice Finance can help.

For businesses of all shapes and sizes

As Australia's most flexible invoice finance provider, we can support businesses that others can't.

If you satisfy the basic requirements below, we'd love to hear from you.

You have an ABN or ACN

You have outstanding invoices with other Australian businesses

You invoice after goods or services have been delivered

Invoice finance is more than a quick fix for cash flow. It’s a way to build resilience, unlock growth, and reduce the financial pressure that comes with long payment terms. It's a much more dynamic cash flow solution than a typical business loan which gives you a cash injection and then years of regular repayments to keep on top of. With Earlypay, you’ll have a partner who’s invested in your success and ready to support your business at every stage.

Whether you know it as invoice finance, debtor finance, invoice discounting, or invoice factoring, it’s all about turning unpaid invoices into cash for your business.

National reach, local support

Earlypay supports businesses right across Australia. From Brisbane, Sydney and Melbourne, to Adelaide, Perth and regional areas in between. We'll help you access funds from your unpaid invoices and keep your cash flow flowing. Our team takes the time to understand your business and provide customised assistance and finance options, no matter where you’re based.

Unpaid invoices are much more than an inconvenience, they can stall your business. Slow customers payments may mean:

Delaying wages or supplier payments

Missing opportunities to expand or take on new contracts

Increasing reliance on credit cards or overdrafts

Added stress for business owners

Invoice finance turns this problem into an opportunity. Instead of waiting for your customers to pay you, Invoice Finance gives you fast access to up to 85% of your outstanding invoice value, keeping your cash flow healthy and your business moving forward.

Why choose Invoice Finance? So you can turn tomorrow’s payments into today’s opportunities.

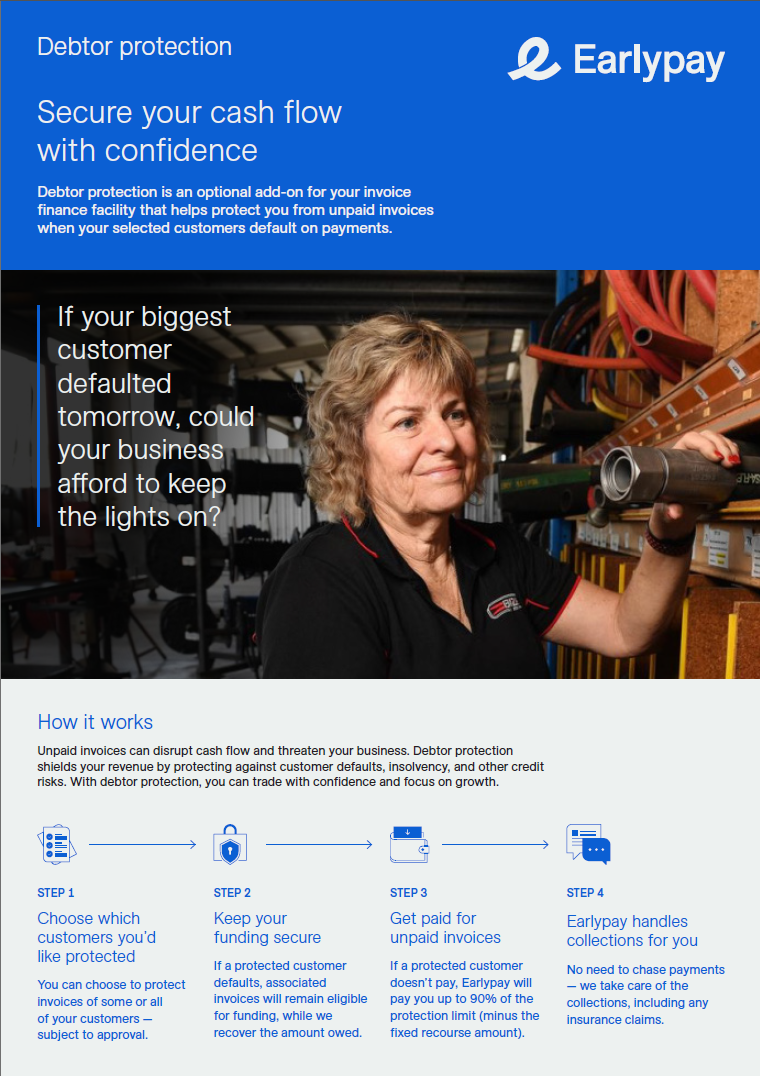

Protect your business from unpaid invoices with Debtor Protection

Even the strongest businesses can face the risk of customers not paying. With Earlypay’s Debtor Protection, you can protect your cash flow and reduce the risk of bad debts.

Peace of mind. Know your invoices are protected, even if your customer defaults.

Protect your growth.Take on bigger contracts with confidence, without worrying about payment risk.

Flexible cover. Choose the level of protection that suits your business.

Debtor Protection is available as an optional add-on to your invoice finance facility, giving you extra security when you need it.

Questions about what Invoice Finance (Debtor Finance) is

What is invoice financing?

Invoice financing (Debtor Financing) is a line of credit that provides funding based on outstanding invoices. Businesses can receive 80% of the value of invoices upfront which increases cash flow that can be used for operational costs or to invest in growth opportunities,

As invoice finance is supporting by outstanding invoices, the amount of available funding grows with your sales and can be used by early-stage, growing and established businesses across a wide range of industries.

What are the Pros and Cons of invoice financing?

Pros

Immediate cash flow

Ongoing access to finance

Backed by invoices, not real estate

High approval rates

No regular fixed loan repayments

Option to outsource collections

Cons

Costs higher than real estate backed finance

What is the difference between Invoice Finance and Debtor Finance?

Nothing. Invoice Financing and Debtor Financing are different names for the same thing. It's also sometimes known as Accounts Receivable Financing.

What is Confidential Invoice Finance (Undisclosed Invoice Finance)?

Confidential Invoice Financing or Undisclosed Invoice Financing is when Earlypay provides funding of your invoices and your customers are not aware that there is a Debtor Factoring facility in place. Confidential invoice financing is generally offered to businesses with a strong track record.

What is Disclosed Invoice Finance?

Disclosed Invoice Finance is the arrangement where your customers are aware that Earlypay is financing your invoices. Disclosed arrangements generally involve Earlypay managing the collection of your invoices and we may contact your customers on your behalf to ensure they pay your invoices. This is a useful arrangement for businesses that have small finance teams or simply choose to outsource this function and focus on other areas of their business.

Disclosed invoice financing is increasingly common in Australia and although some business owners worry about their customers knowing that they use Debtor factoring, it is very rarely an issue. If you do prefer that the factoring arrangement remains confidential, please let your Earlypay representative know.

What is the difference between Invoice Factoring and Invoice Discounting?

Invoice Factoring and Invoice Discounting are the two types of Invoice Financing.

Invoice Factoring (Debtor Factoring) involves a business selling its invoices to the invoice factoring company in exchange for upfront payment for around 80%. When the invoice is paid, the finance with the factoring business is repaid and the balance, less any fees, becomes available to the business that sold/financed the invoice. Invoice factoring is generally disclosed to your customers and the financier can manage collections. Earlypay can however, offer confidential facilities to selected businesses.

Invoice Discounting is different to Invoice Factoring as the invoices are not sold to the invoice financing business but instead used as security for finance. A business can access funding of up to 80% of the value of its outstanding accounts receivable balance. Invoice Discounting is often confidential and the business retains control of invoice collections management making it better suited to larger and more established businesses.

What type of Invoice Financing is right for my business?

Invoice Financing (Debtor Financing) is a very flexible form of business finance that can be tailored to suit the needs of your business. In addition to unlocking cash from unpaid invoices, invoice finance can also include collections management services, allowing businesses to focus resources on other areas.

Invoice Financing is used by businesses across a wide range of industries including Wholesale trade, Transport, Manufacturing, Recruitment, Labour hire, Business services and many others.

Start-ups, Growing and Established businesses are all eligible for Invoice Finance and we’d love to hear from you even if you have a short trading history, less than perfect credit score or ATO debts.

Given the flexible nature of invoice finance, and the fact that every business is different, it's best to speak to our experienced team to design a solution that works best for you and your business.

Questions about how Invoice Financing (Debtor Financing) works

How Invoice Financing works with Earlypay

Invoice your clients as you normally would.

Provide Earlypay with the details of the invoices you would like to fund. (If you use Xero or MYOB AccountRight Live, Earlypay can source your invoice details through our clever integration. If you don't use these online accounting platforms, you can upload the invoice details to our platform.)

Receive up to 80% of the value of your funded invoices upfront.

Your customers pay invoices into a collections account set up in your name which repays the outstanding finance and the excess becomes available to you.

Will my customers know that I'm using Invoice Finance?

Earlypay offers both Confidential (Undisclosed) and Disclosed Invoice Financing services. Typically, established businesses are eligible for Confidential Invoice Finance, and Disclosed Invoice Finance is better suited to businesses that have a short trading history, significant debts or a less than perfect credit history. Earlypay will work with you to tailor the best solution for your business.

How do I access my Invoice Finance facility?

You will be given access to an online portal where you can view your invoices and funding availability, request drawdowns and download reports.

What security do I need to provide for Invoice Financing?

One of the main benefits of Invoice Financing is that it doesn't require real estate security. Funding is advanced against the value of the unpaid invoices and the primary security is the invoices themselves.

Why would I use Invoice Finance (Debtor Finance) instead of an Unsecured Business Loan?

Invoice Financing is generally more flexible than Unsecured Business Loans because you can access funding as and when you need the cash flow. Unsecured Business Loans provide a lump sum amount that is repaid with regular repayments over a fixed term whereas the repayment of Invoice Financing occurs when customers pay the invoices that were financed.

Invoice finance is often more cost effective than unsecured business loans as it uses the accounts receivable ledger of your business as security, making it less risky for the invoice financier.

Business loans require businesses to have been operating for a minimum period and show evidence that the repayments can be adequately covered by revenue. Invoice financing, and specifically Invoice Factoring, can be a great solution for businesses that have invoices eligible for financing but don't quite satisfy the requirements for unsecured business loans.

If you're business has a short trading history, less than perfect credit score or ATO debts, you may still be eligible for invoice financing with Earlypay.

Questions about eligibility for Invoice Financing (Debtor Financing)

Can I use Invoice Financing if I have debt with other lenders?

Yes. We are mainly concerned with having security against your accounts receivable and can work alongside other lenders.

Is Invoice Financing suitable for start-ups?

Yes! We love supporting early stage businesses. If you have outstanding eligible invoices, we can help with the cash flow your business needs to grow with invoice financing.

Can you help if my business has ATO tax debt?

Yes. Invoice Financing can be suitable for businesses that have ATO debts and is often available when other types of business loans are not.

Questions about applying for finance

How do I apply for Invoice Financing?

Applying for Invoice Financing with Earlypay is a quick and easy online process. Simply click the sign-up button above, complete some basic details to get started and an Earlypay representative will contact you ASAP.

If you use Xero or MYOB AccountRight, you can streamline the process by connecting your accounting software to Earlypay. This securely provides financial information that may include invoices, credit notes, bank transactions, payments, profit & loss statement and balance sheet.

How long will it take for my finance to be approved?

If you use one of the compatible online accounting platforms, we aim to let you know within 24 hours if your finance has been approved or not. If you don't use Xero or MYOB AccountRight it can take a little longer depending on how long it takes to get the information together.

How long will it take to receive funding?

We aim to advance funding within 24 hours of approving your finance.

How much finance can I get?

Earlypay provides Invoice Financing facilities from $50k all the way up to $10m so we have the capacity to support businesses of all shapes and sizes. More relevant is the size of your accounts receivable ledger as we can advance 80% (sometimes 90%) of the value of those outstanding invoices. For example, if you have $500k of Eligible Invoices, we can advance up to $400k normally and can make temporary exceptions to advance more than that.

What invoices can I fund?

Invoices eligible for funding are invoices outstanding with Australian businesses for goods that have been delivered or services that have been completed. Typically, Earlypay doesn’t fund invoices that are more than 90 days past the issue date.

How much does Invoice Financing cost?

The interest rate charged on Invoice Financing balances ranges between 7.99% and 13.95% per annum. Depending on how you would like your facility to work and any additional services (eg. collections management), there may also be Drawdown or Administration fees.

Still have questions? Talk to a finance expert today.